Stock Market 101 – Lesson 27: Auditor Report & Qualifications: What’s Normal vs Dangerous

Article Information

Author: Kartalks Education Desk

Reviewed by: Kartalks Editorial Team

Content Type: Stock market education and beginner-friendly finance learning

Sources: SEBI investor education material, NSE/BSE educational resources, official public sources, and general finance learning references

Last Updated: Apr 25, 2026

Hook

Auditor Report & Qualifications: Many beginners read revenue, profit, and EPS first.

Very few stop and ask one simple question:

What did the auditor actually say about these numbers?

That question matters more than most people think. The auditor’s report is a key part of the annual filing, and Investor.gov says most audit reports express an “unqualified opinion” that the financial statements fairly present the company’s financial position in conformity with GAAP. The same Investor.gov guidance also says that if an auditor gives a qualified opinion or a disclaimer of opinion, investors should look carefully at what prevented the auditor from giving a clean opinion.

That is exactly what this lesson is about.

In simple words, an Auditor Report tells you whether the auditor is comfortable with the financial statements, or whether something serious needs extra attention. Some audit comments are normal. Some are caution signs. A few are genuinely dangerous. Learning that difference can save beginners from ignoring the most important warning page in the annual report.

What Is an Auditor Report?

An auditor report is the independent auditor’s formal opinion on the company’s financial statements. Investor.gov notes that the annual report on Form 10-K includes audited financial statements, and the auditor’s report is one of the key parts investors should read.

In practical investing language, the auditor report answers this question:

“Based on the audit work, can the auditor rely on these financial statements enough to issue an opinion?”

That does not mean auditors promise perfection. It means they are giving an opinion on whether the statements are presented fairly, in all material respects, under the applicable framework. PCAOB standards explain that the auditor’s report is the medium through which the auditor expresses an opinion or, if necessary, disclaims an opinion.

Why the Auditor Report Matters for Investors

A company may look attractive on the surface, but the auditor report can reveal whether the numbers come with a clean opinion, an exception, a serious disagreement, or no opinion at all.

Investor.gov explicitly says investors should carefully review qualified opinions, disclaimers of opinion, and even material weaknesses in internal controls over financial reporting. That is a strong hint that the auditor report is not a formality. It is a risk-check page.

So for a beginner, the auditor report is not just an accounting paragraph. It is one of the fastest ways to separate:

- normal reporting

- caution-worthy reporting

- and potentially dangerous reporting

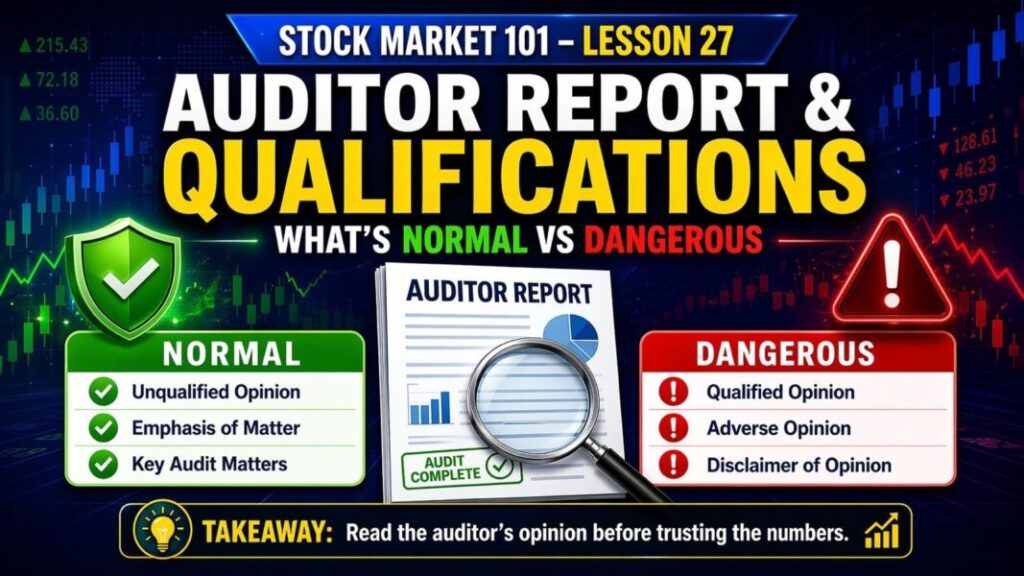

What Is Normal in an Auditor Report?

1. Unqualified Opinion or Unmodified Opinion

This is the “clean” opinion that most investors want to see.

Investor.gov says most audit reports express an unqualified opinion. In everyday use, many modern standards also use the phrase unmodified opinion for the same basic idea: the auditor is not modifying the opinion on the financial statements.

In simple words, this usually means:

- the auditor completed the audit

- did not find a material problem requiring a modified opinion

- and believes the financial statements are fairly presented in all material respects

That does not mean the company is automatically a good investment. It only means the auditor did not see a reason to modify the opinion on the financial statements as a whole. A bad business can still receive a clean audit opinion if the statements are fairly presented. That is an important beginner lesson.

2. Emphasis of Matter Is Not Always a Disaster

Many beginners panic whenever they see extra paragraphs in the report.

That is not always the right reaction.

IFRS material discussing going-concern reporting explains that when adequate disclosure is made in the financial statements, the auditor may still issue an unmodified opinion and include an Emphasis of Matter paragraph to highlight a material uncertainty, such as going concern, that is fundamental to understanding the statements. IFAC also says an emphasis-of-matter paragraph is used when the auditor wants to draw attention to a matter already properly presented or disclosed in the financial statements because it is fundamental to users’ understanding.

So an emphasis paragraph is not automatically the same as a qualification. It often means:

- “The auditor is still giving an unmodified opinion”

- but

- “You should pay very close attention to this disclosed issue”

That is more serious than a routine clean report, but it is not automatically equal to a qualified, adverse, or disclaimer opinion.

3. Key Audit Matters or Critical Audit Matters Are Not Qualifications by Themselves

You may also see a section discussing complex or important audit areas.

Under PCAOB standards, these are called Critical Audit Matters (CAMs), and the PCAOB says they are matters involving especially challenging, subjective, or complex auditor judgment. The PCAOB also clearly states that CAMs are not a substitute for a qualified opinion, adverse opinion, or disclaimer, and they do not alter the auditor’s opinion on the financial statements taken as a whole. IFAC’s materials on ISA 701 similarly explain that Key Audit Matters (KAMs) are matters of most significance in the audit.

This is a very important beginner point:

Seeing CAMs or KAMs does not automatically mean something is wrong. It often means the company had areas requiring deeper audit attention, such as revenue recognition, impairment, or valuation. Read them carefully, but do not confuse them with an audit qualification.

Auditor Report & Qualifications: What Can Be Dangerous in an Auditor Report?

Now let us move to the parts that deserve much more caution.

1. Qualified Opinion

A qualified opinion means the auditor found a material issue, but not one so pervasive that the entire financial statements must be rejected.

ICAI’s UDIN FAQ explains that a modified opinion can be of three types: qualified opinion, adverse opinion, or disclaimer of opinion. PCAOB standards also treat qualified opinions as a departure from an unqualified opinion. Investor.gov says investors should look carefully at what kept the auditor from expressing an unqualified opinion.

For a beginner, a qualified opinion usually means:

- something material is wrong, limited, or unresolved

- but the rest of the statements may still be usable

This is not normal, and it should never be ignored.

2. Adverse Opinion

This is far more serious.

PCAOB AS 3105 says an adverse opinion means the financial statements do not present fairly the company’s financial position, results of operations, or cash flows in conformity with the applicable accounting principles.

In plain English:

This is the auditor saying the financial statements are materially wrong in a broad enough way that investors should not treat them as fairly presented.

That is usually a major red flag for any beginner investor.

3. Disclaimer of Opinion

A disclaimer of opinion is also very serious.

PCAOB standards state that a disclaimer means the auditor does not express an opinion on the financial statements. ICAI’s guidance also lists disclaimer as one of the three forms of modified opinion.

This usually means something like:

- the auditor could not obtain enough appropriate evidence

- or the limitation was severe enough that the auditor would not issue an opinion

For a beginner, this is dangerous because the auditor is not backing the statements with an opinion at all.

What Is More Dangerous: Qualified, Adverse, or Disclaimer?

A simple beginner ranking is:

Least severe of the three: Qualified opinion

More severe: Adverse opinion

Also very severe: Disclaimer of opinion

Why?

Because a qualified opinion says there is a material problem, but the issue may be limited to a specific area. An adverse opinion says the statements as a whole are not fairly presented. A disclaimer says the auditor is not even giving an opinion.

So if your readers ask what is truly dangerous, the answer is simple:

Adverse and disclaimer opinions deserve the most caution. Qualified opinions also matter and should never be brushed aside.

Material Weaknesses: Another Warning Sign Investors Should Not Ignore

Investor.gov also says investors should carefully evaluate material weaknesses disclosed on internal controls over financial reporting.

That matters because even if the opinion on the financial statements is not modified, weak internal controls can still signal problems in how the company records, reviews, and safeguards its financial reporting process. For beginners, this is a reminder that reading only the opinion line is not enough. You should also check whether the report or annual filing mentions serious control issues.

How to Read Auditor Report Language Like a Beginner

Here is a simple method.

Step 1: Find the opinion first

Check whether it is unqualified/unmodified, qualified, adverse, or disclaimer. Investor.gov specifically highlights these distinctions for readers of annual filings.

Step 2: Read the basis paragraph

If there is a qualified, adverse, or disclaimer opinion, the basis paragraph tells you why. PCAOB and ICAI standards frame these as formal modifications to the opinion, so the reason matters a lot.

Step 3: Do not confuse emphasis or CAM/KAM with a qualification

An emphasis paragraph may still come with an unmodified opinion, and CAMs/KAMs do not change the opinion by themselves.

Step 4: Check internal control disclosures

Material weaknesses deserve extra attention even if the main opinion looks clean.

Step 5: Match the report with the rest of the annual filing

If management is very optimistic but the auditor report contains a modified opinion or serious warning language, believe the caution, not just the promotional tone. That is an inference, but it is the sensible way to read the filing.

Indian Market Note: Why Audit Qualifications Matter Even More

For Indian listed entities, SEBI requires annual audited financial results to be submitted with the audit report and a Statement on Impact of Audit Qualifications when there is a modified opinion. SEBI’s rules also say that where the audit report carries an unmodified opinion, the listed entity must furnish a declaration to that effect to the stock exchanges while publishing annual audited financial results.

That means audit qualifications are important enough in the Indian market that exchanges and investors are expected to see their impact clearly. For beginners, that is another strong signal not to ignore them.

Final Lesson Summary

The biggest takeaway from this lesson is simple:

A clean auditor report is normal. A modified auditor report needs attention. An adverse opinion or disclaimer can be dangerous.

Most audit reports are unqualified or unmodified. That is the normal starting point. But when you see a qualified opinion, an adverse opinion, a disclaimer, or serious control weakness language, you should stop and read carefully. Investor.gov, PCAOB, ICAI, and SEBI all support the idea that these audit signals matter and are not just technical accounting language.

For long-term investors, this lesson is powerful because it teaches one habit:

Do not just read the profits. Read what the auditor thinks about them.

5 FAQs – Auditor Report & Qualifications

1. What is the normal auditor opinion investors usually see?

Most audit reports express an unqualified opinion, which Investor.gov describes as the usual clean opinion stating that the financial statements fairly present the company’s financial position in conformity with GAAP.

2. Is an emphasis of matter always dangerous?

Not always. Official guidance explains that an auditor can still issue an unmodified opinion and include an Emphasis of Matter paragraph to highlight an important disclosed issue that is fundamental to understanding the financial statements.

3. What is a qualified opinion in simple words?

A qualified opinion means the auditor found a material issue, but not one so pervasive that the whole financial statements must be rejected. It is a modified opinion and should be taken seriously.

4. Which is more dangerous: adverse opinion or disclaimer?

Both are very serious. An adverse opinion says the financial statements do not present fairly, while a disclaimer means the auditor is not expressing an opinion at all.

5. Are CAMs or KAMs the same as audit qualifications?

No. PCAOB says critical audit matters do not alter the auditor’s opinion and are not a substitute for a qualified opinion, adverse opinion, or disclaimer. IFAC describes key audit matters as matters of most significance in the audit, not automatic qualifications.

Further reading

Stock Market 101 – Lesson 26: Management Discussion (MD&A): How to Read Promoter Confidence

Stock Market 101 – Lesson 25: Notes to Accounts: Hidden Clues Most People Ignore

Stock Market 101 – Lesson 24: Cash Flow Statement in Real Life: Profit vs Cash (Red Flags)

Stock Market 101: Learn Stocks from Zero

Disclaimer

This lesson is for educational purposes only and should not be treated as investment advice. Please do your own research before making any investment decision.