Stock Market 101 – Lesson 35: Mutual Fund Metrics Made Simple: Expense, Rolling Returns, Risk

Hook

Many beginners choose mutual funds by looking at one number only: past return.

If a fund shows 25% return, it looks attractive.

If another fund shows 12% return, it looks less exciting.

But this is where many new investors make a mistake.

A mutual fund should not be judged only by return. You must also understand the cost, consistency, and risk behind that return. That is exactly why Mutual Fund Metrics are important.

Think of it like buying a car. You do not check only the speed. You also check mileage, maintenance cost, safety, comfort, and reliability. In the same way, before choosing a mutual fund, you should look at important metrics like expense ratio, rolling returns, riskometer, standard deviation, beta, and Sharpe ratio.

This lesson will explain these terms in simple words, without making it feel like a finance textbook.

Mutual Fund Metrics: Simple Meaning

Mutual Fund Metrics are numbers and indicators that help investors understand a fund better.

They help answer simple questions like:

- Is this fund costly?

- Is the performance consistent?

- Is the fund taking too much risk?

- Is the return good compared to the risk?

- Is the fund suitable for my goal?

These metrics do not guarantee future returns. They only help you make a more informed decision. AMFI clearly says mutual fund schemes are not guaranteed or assured return products, and mutual fund units involve investment risks.

So, the goal is not to find a “perfect” fund.

The goal is to avoid choosing blindly.

Why Beginners Should Learn Mutual Fund Metrics

A beginner may ask, “Why should I learn all these numbers? Can’t I just choose a good fund?”

The problem is that a fund may look good from outside but may not suit your risk profile.

For example:

- A fund may show high return because it took very high risk.

- A fund may perform well only in one market phase.

- A fund may have a high expense ratio.

- A fund may fall more sharply than similar funds.

- A fund may not be consistent across different time periods.

That is why beginners should not depend only on one-year return or social media suggestions. AMFI’s investor disclaimer also reminds investors that past performance is not necessarily indicative of future performance.

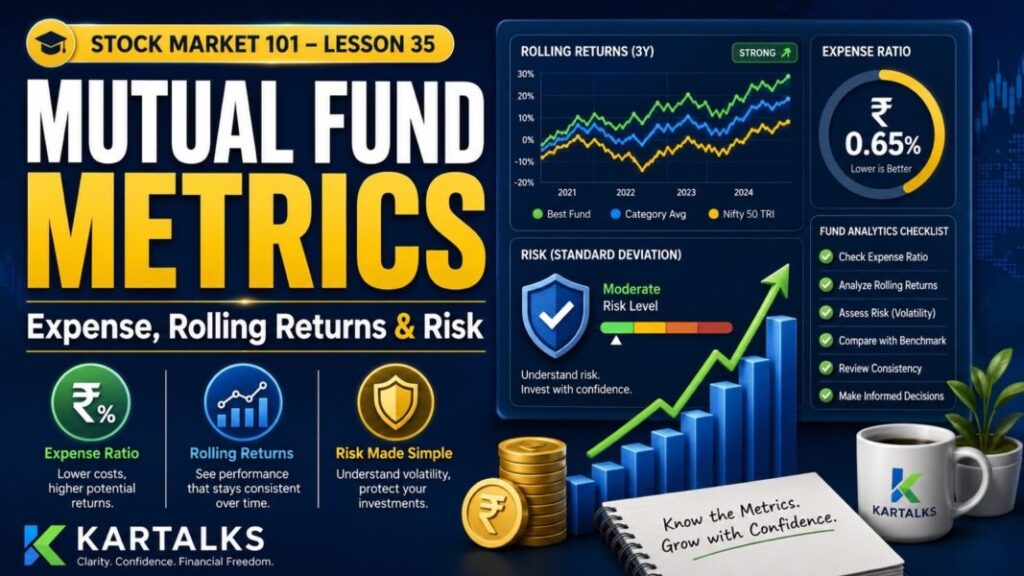

1. Expense Ratio: The Cost of Owning a Fund

The expense ratio is one of the easiest mutual fund metrics to understand.

It is the cost charged by the mutual fund for managing the scheme. This cost includes fund management, administration, operations, and other scheme-related expenses.

AMFI explains that Total Expense Ratio, or TER, is calculated as a percentage of the scheme’s average Net Asset Value, and daily NAV is disclosed after deducting expenses.

Simple example

Suppose two similar funds generate the same gross return.

But:

- Fund A has a lower expense ratio

- Fund B has a higher expense ratio

Over time, the lower-cost fund may keep more return in the investor’s hand, assuming all other things are similar. SEBI’s investor education page gives a simple example showing how a lower expense ratio in a direct plan can improve effective returns compared with a higher-cost regular plan.

Why expense ratio matters

Expense ratio matters because it directly affects your net return.

A small difference may not feel big in one month.

But over many years, cost can compound.

That does not mean the cheapest fund is always the best. A low-cost fund with poor strategy or poor tracking may still disappoint.

So use expense ratio wisely:

- Compare funds within the same category.

- Do not compare a liquid fund with a small-cap fund.

- Do not choose only because the expense ratio is low.

- Check cost along with performance and risk.

2. Regular Plan vs Direct Plan

This is closely connected to expense ratio.

A regular plan usually includes distributor commission.

A direct plan does not include distributor commission.

Because of this, direct plans generally have a lower expense ratio than regular plans. AMFI explains that the lower expense ratio of direct plans can translate into higher returns over time compared with regular plans of the same scheme.

Beginner point

If you invest through an advisor or distributor, you may be in a regular plan.

If you invest directly through the AMC website or direct platforms, you may be in a direct plan.

Both have a place.

If you need guidance, a regular plan with proper advice may be useful. If you can research and manage your investments yourself, a direct plan may reduce cost.

The important thing is to know what you are choosing.

3. Rolling Returns: Better Than Only One-Year Return

Many beginners check only 1-year, 3-year, or 5-year return.

This is called point-to-point return.

It tells you what happened between two dates.

But the problem is simple: returns can look very different depending on the start date and end date.

That is where rolling returns become useful.

Rolling returns show how a fund performed across many different time periods, not just one fixed start and end date. Mutual Fund Sahi Hai explains that rolling returns indicate average annualised returns calculated for a given time frame and can give a smoother view of performance across different periods.

Simple example

Instead of asking:

“How much did this fund return from January 2021 to January 2026?”

Rolling return asks:

“How did this fund perform across many 3-year or 5-year periods?”

This gives a better idea of consistency.

Why rolling returns are useful

Rolling returns help beginners check:

- whether performance is consistent

- whether the fund did well only in one lucky period

- how the fund behaved across different market phases

- whether the fund regularly beats its benchmark or category

For long-term investors, rolling returns are often more useful than just one-year return.

4. Riskometer: The First Risk Check

Before investing in any mutual fund, beginners should check the Riskometer.

SEBI explains that the Riskometer is a risk-measuring tool used in the mutual fund industry to show the risk level of a scheme, and it is mandatory for AMCs to display it. It shows risk from low to very high.

Why Riskometer matters

Many fund names sound safe.

But the actual risk may be higher than expected.

For example:

- a small-cap fund may show very high risk

- a sector fund may show high risk

- a long-duration debt fund may carry interest-rate risk

- a credit-risk fund may carry credit-quality risk

The Riskometer gives a quick first-level warning.

It does not tell the full story, but it is a good starting point.

Beginner rule

If the Riskometer says high or very high risk, do not ignore it.

Ask yourself:

- Can I handle this risk?

- Is my time horizon long enough?

- Will I panic if the fund falls?

- Does this fund suit my goal?

5. Standard Deviation: How Much the Fund Moves

Standard deviation sounds technical, but the meaning is simple.

It shows how much a fund’s returns move up and down from its average.

A fund with higher standard deviation usually has higher volatility.

A fund with lower standard deviation usually behaves more steadily.

Mutual Fund Sahi Hai explains risk indicators such as beta and Sharpe ratio, and risk analysis commonly uses volatility-related measures to understand how a fund behaves compared with the market.

Simple example

Imagine two funds.

Fund A gives returns like this:

- 10%

- 11%

- 9%

- 12%

- 10%

Fund B gives returns like this:

- 25%

- -10%

- 30%

- -5%

- 20%

Both may look good in some years, but Fund B is clearly more volatile.

That is what standard deviation helps you understand.

Beginner use

Use standard deviation to check:

- how volatile the fund is

- whether the volatility suits your comfort

- whether the fund is taking too much risk for returns

- whether similar funds are smoother

Do not use this number alone. Use it with returns, category, and risk profile.

6. Beta: How the Fund Moves Compared to the Market

Beta tells you how sensitive a fund is compared to the market.

Mutual Fund Sahi Hai explains that beta measures a fund’s volatility with respect to the market. A beta above 1 means the scheme may be more volatile than the market, while beta below 1 means it may be less volatile than the market.

Simple meaning

- Beta of 1: fund moves broadly like the market

- Beta above 1: fund may move more aggressively than the market

- Beta below 1: fund may move less than the market

Simple example

If the market falls 10%, a fund with high beta may fall more.

If the market rises 10%, the same fund may also rise more.

So beta is not automatically good or bad.

It only tells you how sensitive the fund is.

Beginner use

Beta is useful when comparing equity funds.

But beginners should not choose a fund only because beta is low or high.

A high-beta fund may suit aggressive investors.

A lower-beta fund may suit investors who want relatively calmer movement.

7. Sharpe Ratio: Return Compared to Risk

The Sharpe ratio is a popular metric for risk-adjusted return.

In simple words, it tells you whether the fund is giving enough return for the risk taken.

Mutual Fund Sahi Hai explains that Sharpe ratio measures the excess return provided by a fund per unit of risk undertaken and is a useful indicator of risk-adjusted return.

Simple example

Two funds give 12% return.

But:

- Fund A took lower risk

- Fund B took very high risk

Which one is better?

The answer may be Fund A, because it achieved the same return with less risk.

That is what Sharpe ratio helps you understand.

Beginner use

A higher Sharpe ratio is generally better when comparing similar funds.

But again, use it carefully.

Do not compare:

- equity fund Sharpe with liquid fund Sharpe

- small-cap fund Sharpe with debt fund Sharpe

- sector fund Sharpe with large-cap fund Sharpe

Compare funds within the same category.

8. Alpha: Did the Fund Beat the Benchmark?

Alpha tells you whether the fund performed better or worse than its benchmark after considering risk.

For beginners, the simple question is:

Did the fund add value compared with the benchmark?

If a fund is actively managed, investors usually expect it to do better than the benchmark over time.

If it cannot do that consistently, then investors may ask whether the higher expense ratio is justified.

Beginner use

Alpha is useful, but do not check it for one short period only.

Look at:

- rolling performance

- different market phases

- consistency

- category comparison

- risk taken to generate return

A good fund should not only beat the benchmark once. It should show a sensible pattern over time.

9. Fund Performance vs Category Average

Beginners should avoid checking one fund alone.

Always compare the fund with:

- its benchmark

- its category average

- similar funds

- rolling performance

- downside performance

If a fund gave 14% return, that may look good.

But if the category average was 18%, then the fund may not be impressive.

If a fund gave 10% return when the category gave 4%, that may be strong.

Context matters.

That is why mutual fund metrics should always be read together.

10. Downside Protection: How the Fund Falls

This is one metric beginners often ignore.

Everyone likes to see how much a fund rises.

But smart investors also ask:

How much does this fund fall when the market falls?

A fund that rises fast but falls even faster may not suit every investor.

Check these questions

- Did the fund fall more than its category during corrections?

- Did it recover faster or slower?

- Was the fall due to market conditions or poor stock selection?

- Is the fund too concentrated?

This is especially important for beginners who may panic during market corrections.

11. Portfolio Turnover: How Often the Fund Changes Holdings

Portfolio turnover shows how frequently the fund manager buys and sells securities.

A high turnover may mean the fund is more active.

A low turnover may mean the fund follows a more stable holding style.

High turnover is not automatically bad. Low turnover is not automatically good.

But beginners should ask:

- Is the fund manager changing too often?

- Is the strategy consistent?

- Are frequent changes increasing costs?

- Does the fund still match its objective?

This metric is more useful for investors who want to understand the fund’s style.

12. Expense, Return, and Risk: Read Together

This is the most important part of the lesson.

Do not read mutual fund metrics separately.

Read them together.

A good fund is not just:

- highest return

- lowest expense

- lowest risk

- highest Sharpe ratio

A good fund is one that fits your goal and delivers performance with a risk level you can handle.

Simple beginner checklist

Before choosing a fund, ask:

- Is the expense ratio reasonable?

- Are rolling returns consistent?

- What does the Riskometer say?

- Is volatility comfortable for me?

- Is beta too high for my risk profile?

- Is Sharpe ratio good compared to similar funds?

- Did the fund perform well across market cycles?

- Am I choosing this fund only because of past return?

This checklist can save beginners from many common mistakes.

Common Mistakes Beginners Make

1. Choosing only by 1-year return

One-year return can be misleading.

It may be affected by one sector rally, one market phase, or one lucky period.

2. Ignoring expense ratio

Costs look small but matter over long periods.

3. Ignoring risk

A fund that gives high return may also carry high risk.

4. Comparing wrong categories

Do not compare small-cap funds with liquid funds.

Do not compare sector funds with balanced funds.

Compare similar funds only.

5. Thinking past return will repeat

Past performance is not a guarantee. Mutual Fund Sahi Hai clearly says past performance is not necessarily indicative of future performance.

6. Ignoring personal suitability

A fund may be good, but it may not be good for you.

Your goal, time horizon, and risk comfort matter.

Mutual Fund Metrics: Final Learning

The final learning is simple.

Mutual Fund Metrics help beginners see beyond returns.

Expense ratio tells you the cost.

Rolling returns tell you consistency.

Riskometer tells you the broad risk level.

Standard deviation tells you volatility.

Beta tells you market sensitivity.

Sharpe ratio tells you return per unit of risk.

But no single number is enough.

A beginner should look at the full picture.

The best mutual fund for you is not always the fund with the highest return. It is the fund that matches your goal, time horizon, and risk comfort.

That is how you use mutual fund metrics wisely.

5 FAQs – Mutual Fund Metrics

Q1. What are Mutual Fund Metrics?

Mutual Fund Metrics are numbers and indicators that help investors understand cost, return, consistency, and risk before choosing a fund.

Q2. Why is expense ratio important?

Expense ratio is important because it directly reduces the fund’s net return. Lower cost can help over time, but it should not be the only factor.

Q3. What are rolling returns?

Rolling returns show fund performance across many time periods and help investors judge consistency better than one fixed return period.

Q4. What does Riskometer show?

Riskometer shows the risk level of a mutual fund scheme, ranging from low to very high. SEBI says AMCs must display it for mutual fund schemes.

Q5. Is Sharpe ratio useful for beginners?

Yes, Sharpe ratio can help beginners understand whether a fund is giving reasonable return for the risk taken, but it should be compared only with similar funds.

Further Reading

Stock Market 101 – Lesson 34: How to Choose a Mutual Fund

Stock Market 101 – Lesson 30: Defensive vs Cyclical Sectors

Stock Market 101 – Lesson 25: Notes to Accounts: Hidden Clues Most People Ignore

Stock Market 101 – Lesson 20 Your 12-Month Wealth Plan & Rebalancing

Disclaimer

This article is only for educational and informational purposes. It is not investment advice or a mutual fund recommendation. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully and consult a certified financial advisor before making investment decisions.

Article Information

Author: Kartalks Education Desk

Reviewed by: Kartalks Editorial Team

Content Type: Stock market education, beginner-friendly investing concepts, finance learning, and investor awareness

Sources: SEBI investor education material, NSE/BSE educational resources, official public sources, and general finance learning references

Last Updated: May 16, 2026